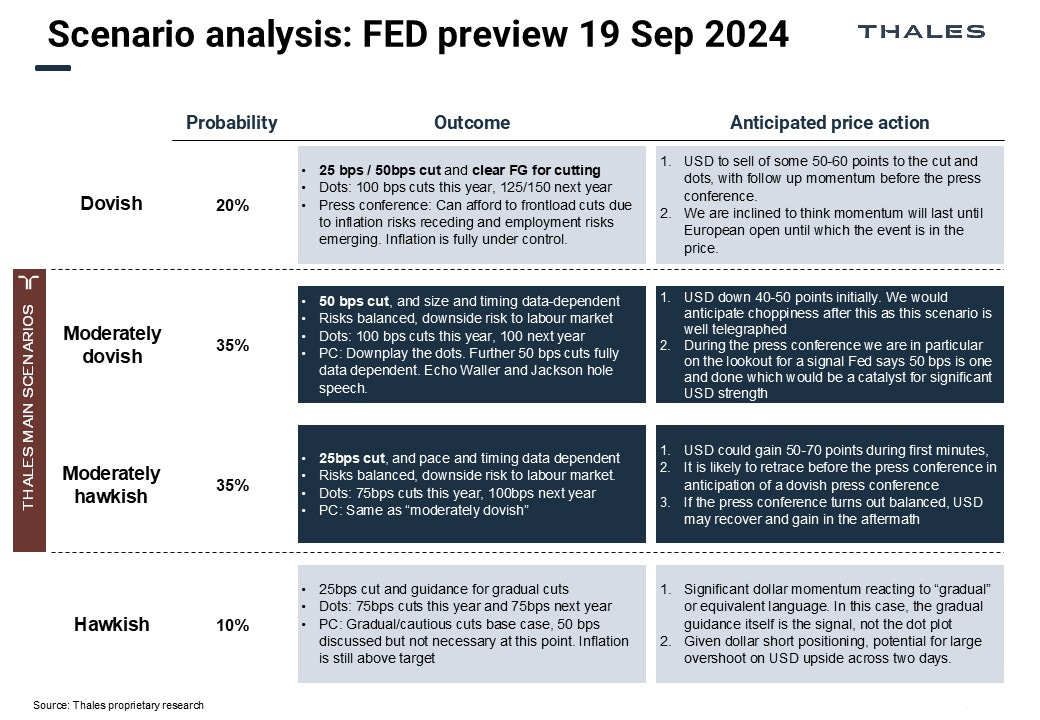

Fed September Preview – Don’t be mislead by the 25 – 50 bps debate

Hello and welcome to our “Fed Preview”. The Fed is embarking on a consequential and historic decision with the kickoff of a cutting cycle. The question on everyone’s lips is that, will it be 25 bps or 50 bps? We think that debate is misleading and that the devil is in the details. This preview covers realistic scenarios for the Fed decision and distils the most important information for your convenience. We aim to also predict the intraday reaction of USD dollar index (DXY) to the decision. We have gone through the investment bank research on the subject and don’t think there are as detailed scenarios in the market.

Executive summary

The market is pricing roughly a 60% chance of a 50 bps cut. The initial volatility will be higher than usual for the Fed because the Fed has done an uncharacteristically poor job communicating whether the cut is 25 or 50 bps.

Don’t be misled by the 25 or 50-bps debate. While it will determine the initial market reaction in the first minutes, it’s the guidance, view on labor markets, and impression of the end destination that matters.

The Fed is expected to keep the door wide open for 50 bps cuts. Any suggestion that a 50 bps cut was one and done or reluctance to embark on a series of 50 bps cuts would be hawkish. Openness to cut in line with market pricing is very dovish, regardless of the size of the cut.

We think EURUSD is a secure play to go long against a dovish Fed, given ECB and Fed divergence (convergence). On the contrary, on a particularly hawkish Fed, we would expect high-beta currencies like AUDUSD to trade weaker (you want to short the weakest horse!).

We think JPY at these levels, though volatile, is quite unpredictable, as demonstrated by the reaction to the Non-farm payrolls report and Waller's speech on Friday 4.9. With NFP, we saw some JPY strength in the aftermath despite ebbing 50 bps odds at the time as the stock market corrected lower.

Jargon explainer

Dot plot: Fed officials' predictions on the future rate path are notoriously unreliable, and the Fed (and economists) often downplay the impact.

FG: Forward guidance. Verbal guidance on what size of rate moves the market can expect in the future.

PC: Press conference. The press conference is 30 minutes after the statement and can cause a re-assessment of the statement. In particular, Fed often balances a hawkish statement with a dovish press conference.

Hi SCX,

Thanks for the comment! Its a bit provocative for sure, yet there's no question most market market commentators don't actually trade the events "live" they comment on, nor do they provide a track record. In my book, market related opinions are not worth much if you don't put your money where your mouth is.

Best,

Aatu

Hello! Aatu Kokkila,

I subscribed today to your new Substack. I was surprised by these last sentences in your welcome email.

[What sets this Substack apart from others is the focus on macro news events. Despite every trader being constantly bombarded by market-moving headlines, there are surprisingly few authorities with a track record commenting the events.]

Best wishes!