NFP Preview – Never mind the hype, see you in November

Since August’s surprise rise in the unemployment rate and the subsequent market reaction in both stocks and the unravelling of carry trade in JPY, the US labour market’s data has become the most important economic news piece for the markets. For this specific report, however, we think the high probability tradeable scenarios are fade trades. Regardless, we are prepared for any outcome.

The underlying logic is that there is one more NFP before the Fed decides on rates, and most importantly the US presidential election is also before the event. We also think a slowly cooling, but not collapsing, labour market is well in the price, so a strong report is unlikely to change the existing narrative much, albeit might cause some short-term USD momentum.

Executive summary

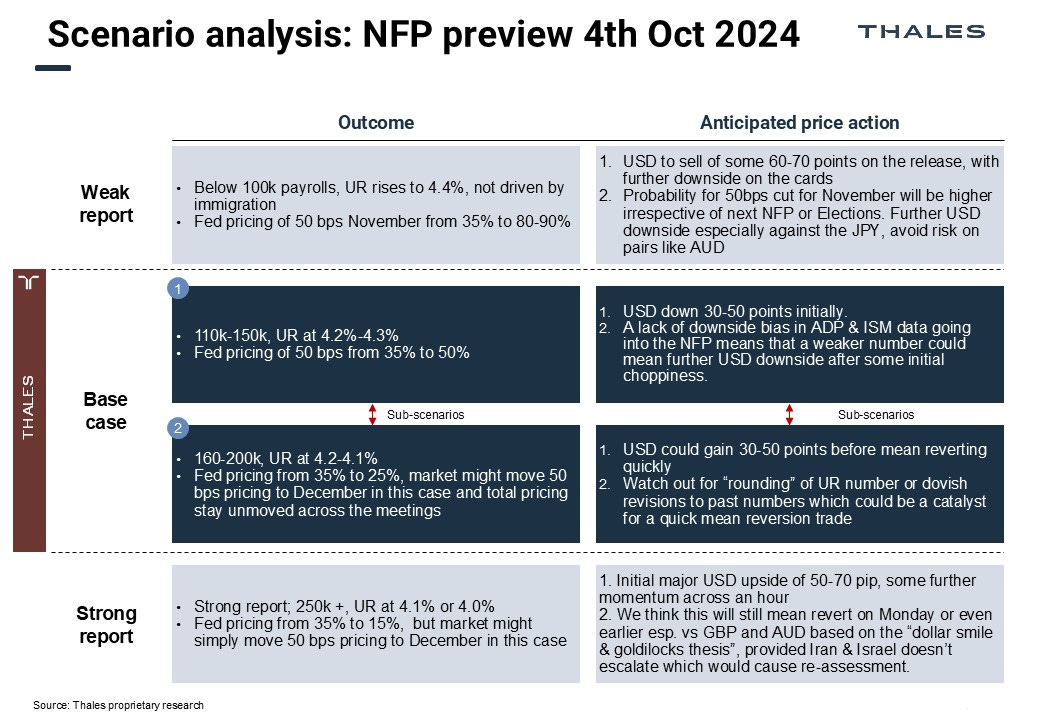

The Fed has communicated that they do not welcome more softness in labour markets and that the attention has shifted from inflation to labour market data making the market ultra-sensitive for weak reports.

The market is pricing 35% odds of a 50bp cut at the November meeting. For the whole year around 70 bps is priced, so almost an 80% chance of a total of another 50bp cut. The market could easily pass the pricing of November to December on a slightly stronger report.

With NFP, it's always important to watch preceding data like unemployment claims, ADP, services, and manufacturing for guidance. This time, the data has been relatively solid, suggesting there’s no downside bias to the number (like there was the last time). On the previous NFP, you saw aggressive USD gains as the market had priced even weaker numbers than the consensus!

We, therefore, think the market has priced to some degree a good number, so truly a weak report, e.g. unemployment at 4.4% driven by genuine weakness in the labour market (e.g. not immigration) would come as a shock and be very USDJPY negative.

We don’t think a strong headline or an unemployment rate of 4.1% is a game-changer at this stage. Watch out for a rounded number on the unemployment rate! It could easily round to 4.3% from 4.25% and be driven by immigration. This would be noise.

Iran and Israel headline risk

The headlines have been dominated by geopolitical news thus far this week. The Markets and the world are looking closely at the situation in the Middle East for further developments. Therefore, we must be mindful of headline risk when trading the NFP (though not exaggerate it!).

We are agnostic on developments. Unless there are no major casualties on either Iran or Israel's side, the information should not cause sustained market reactions in FX. For example, after the Iran retaliation earlier in the week, Crude oil gained, but USDJPY stayed choppy while EURUSD went down which we think was a move driven by the repricing of an ECB October cut.

Regardless, as a rough heuristic, an escalation is USD positive, de-escalation negative. We do not consider this very tradeable on FX alone, but for someone monitoring energy instruments, it is more interesting and of course, if you have short-term positions you must be aware of the risk!

Therefore, we stay on the lookout. A direct Israel strike on Iranian oil fields would escalate the situation, and we would not like to be short dollar in that environment.

Conclusion

It is important to note when it is “game on” and when not, and this time we think it isn’t. There is plenty of data before the Fed’s meeting, so unless the report comes in very weak, we believe the outcome is ultimately mean-reverting.