Reviewing the FOMC & the BOJ

FOMC Review – Frustrating progress on inflation

The Fed was consistent with our hawkish scenario, with a statement pointing to two cuts next year, discussion on upside risks to inflation. The inflation projection for 2025 was also particularly hawkish. As we outlined in the preview, such a statement would be a harbinger for a hawkish press conference.

The press conference included some fresh and unexpected hawkish commentary from Powell like; rate cut today was a “closer call”, and “It's been frustrating, progress on inflation is slower than hoped” and most importantly “need to see further progress on inflation to cut”. The market prices only 30 bps of cuts next year as a result.

We went aggressive dollar long after the statement, given market didn’t understand the details of the statement. Overall, it was the most hawkish Fed press conference since June 2021. USD gained 40 pips in the first minute and then continued up over total 130 points until finding a new level. However, although the USD positioning is extremely crowded, we didn’t expect the dollar to mean revert as quickly as it did.

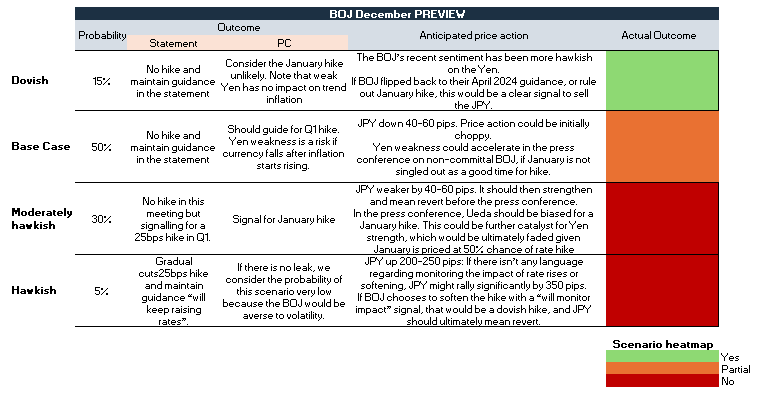

BOJ Review – Lip service on future tightening

The BOJ was very close to our dovish scenario, if not fully. Reading in between the lines, Ueda communicated a very high bar for January hike or future tightening at all and as a result the JPY collapsed over three big figures. The important comments included “Need more data to hike”, need to gauge situation for “quite a while”, require “considerable clearer picture on Trump policies”.

While some analysts highlighted post event that the door was left open to hikes with “need one more notch of data”, to us its very clear is an extremely high bar because there’s no way there’s a lot of clarity in January about Trump’s policies nor will there be a lot of data until the March hike negotiations!

We feel that the 3 big figure move on the JPY Thursday can also be explained partially by pent up Fed impact. JPY was the second strongest G10 currency after the Fed, potentially as traders didn’t want to risk it into the BOJ meeting and due to weak equity markets.

Some may argue JPY is going to be strong if equities are weak, but we don’t buy that. What JPY needs to strengthen is a weaker growth & disinflation, precisely what was happening during the carry trade mini JPY strengthening regime. Our argument is based on 2022 price action, JPY was by far the weakest G10 currency despite market pricing a recession at point (which never happened) because inflation was rising so fast.

We usually don’t like to make predictions, but since all the information is known to everyone until January, we think USDJPY will be pulled like a magnet to 160 and 165. We think there’s a high chance of an intervention in January.

On intervention language, there was a verbal warning from currency diplomat Mimura with the comment “gravely concerned over FX moves” on Friday. There will be a lot of verbal warnings like this, which we think are noise until we trade above 165. The intervention bar should be higher, perhaps at 165 or 170 since JPY is weak vs the USD only. Moreover, the MOF might be more strategic about it than previously, for example, timing after some USD negative news or illiquid times.

PARTING WORDS

Our research experiment has reached an inflection point now and in January, we will reflect on our content and how we shall proceed with this in the future. We truly hope you have found this content valuable and we wish you all a great holiday period!